The Next Escondida — A Copper Mining Play That Will Fund Your Retirement

Metals & Mining

Now, those unfamiliar with mining are probably wondering: “What da fook is Escondida?” You might think it is the name of a Netflix narco drama, but no, it is actually the largest copper mine in the world. Jointly owned by mining behemoths BHP and Rio Tinto, Escondida sits in the Atacama Desert in Northern Chile and quietly produces over a million tonnes of copper a year. At today’s copper prices, that is US$10B+ per year. When Escondida sneezes, the entire copper market catches a cold.

Every mining major is in search of the next Escondida, especially as copper becomes the newest hot commodity driving the global energy transition. I believe there is an exploration company located right in the heart of the Atacama Desert in Northern Chile that has all the makings of the next Escondida. This company is ATEX Resources (TSXV: ATX / OTCQB: ATXRF).

When analyzing a mining play, most people start by looking at resource estimates. They see huge numbers, FOMO in, and then end up bag holding for years while nothing happens. The reality is that mining is almost entirely a people’s business. Great people build great mines. A deposit might look good on paper, but without the right people believing in it and the right connections to advance it, the stock will go nowhere. I believe the following factors, ranked from most important to least, are what you need to look for in a potential multibagger junior mining play:

Investors: Who is backing the junior miner? Tier 1 investors and/or mining majors? Or some “strategic investor” from China with no real mining experience and no track record of actually building anything.

Jurisdiction: Anything in Africa or China? Stay the fook away, unless you enjoy donating money to governments you can’t pronounce or watching your ‘world-class asset’ get repossessed faster than your buddy’s leased BMW.

Management: This will almost always be closely tied to the lead investors. Tier 1 investors and mining majors will bring in experienced operators from their network to lead the company.

Asset: Yes, the actual asset itself is the absolute last thing you need to look at. Screw up the first three and all you’ve got is some rocks in the desert and a CEO with a drone taking promo videos.

Investors

Now, back to ATEX. Starting with the investors. ATEX’s top shareholder is Agnico Eagle, Canada’s biggest and best gold miner — and arguably one of the best operated mining companies in the world. In October 2024, Agnico did a C$55M private placement in ATEX at C$1.63. This came as a bit of a surprise to the mining world as Agnico is known to invest in ultra safe jurisdictions — their mines are in Finland, Canada, and Australia. As part of this deal, Agnico received a ton of warrants at an exercise price of C$2.50. These warrants are exercisable within the next five years. However, there was an extremely important clause in that deal: From and after January 1, 2026, if the volume weighted average price of ATEX’s Common Shares exceed C$3.00 for 20 consecutive trading days, ATEX shall have the right to accelerate the expiry date of the Warrants to 30 calendar days from the date that notice is provided. In simple terms, this means that Agnico must exercise their warrants if ATEX’s share price averages more than C$3.00 for 20 trading days in a row starting in 2026, otherwise they will lose these warrants. Based on this alone, I think ATEX’s share price will surge past C$3.00 as we head into Q1. Agnico will definitely exercise their warrants, ATEX gets additional cash to fund Phase VI exploration, and the headline “Agnico exercises warrants and ups stake to ~20% in ATEX” will hit the front page of The Northern Miner.

Alongside Agnico, Pierre Lassonde is a major shareholder of ATEX. He is the best mining investor in the world. He cofounded Franco Nevada and has backed several juniors that have done incredibly well, with Orla Mining being the latest. He owns 10% of ATEX on a non-diluted basis.

Jurisdiction

Chile is a generally safe jurisdiction. If it is good enough for Agnico, which prides itself on operating in safe jurisdictions, it is good enough for us. Now, just a bit more on the actual location: The Atacama desert hosts several copper gold porphyry deposits at various stages of development including, Filo del Sol (Filo Mining), Josemaria (Lundin Mining), Los Helados (NGEX Minerals/JX Nippon), La Fortuna (Teck Resources/Newmont) and El Encierro (Antofagasta/Barrick Mining). Look at the Tier 1 miners already operating in ATEX’s backyard. In fact, ATEX’s Valeriano project is only 6 km from El Encierro, a joint venture between mining majors Antofagasta and Barrick.

Management

Experienced team. ATEX recently added Elijah Tyshynski as CFO, fresh off the O3 Mining sale to Agnico Eagle. If Agnico exercises its C$2.50 warrants, its stake lands just under 20%. Elijah literally just helped sell a junior to Agnico, so he knows exactly which inbox the term sheet goes to. I think there could be a part two here... more on that later.

Asset

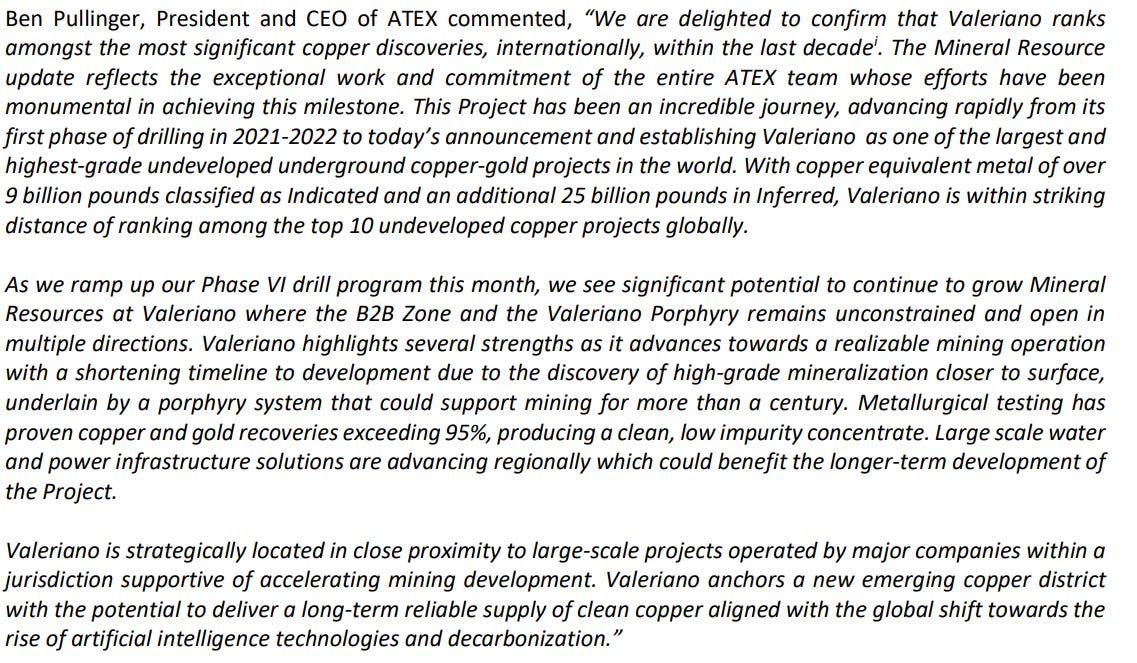

The first three checks are huge green flags. Massive. ATEX’s asset is massive too. I do not want to bury you in geology, so here is a quick snippet from ATEX’s September 23, 2025 PR:

Bottom line, the potential is mind-boggling, and I believe this is/will become one of the biggest copper mines in the world.

If you don’t believe me, hear it from Pierre Lassonde himself (fast forward to 39:00):

He said it’ll be bigger than NGEX. Look at NGEX’s chart.

Fast forward to 54:30 of this interview too: https://x.com/GoldTelegraph_/status/1867307651031261417?s=19

Make sure you listen to both snippets.

Outlook

ATEX should uplist to the TSX before year end. This opens the door for large funds to buy, buy, buy. And let me tell you, a ton of large funds made a ton of money off the recent run Orla Mining had. They’ll be looking to redeploy their gains into another Lassonde baby. Also, ATEX recently uplisted in the US and liquidity has immensely improved for American investors.

I expect the stock to surge past C$3.00 heading into Q1. If you look at historical charts, it typically catches a bid in the fall. I think after they complete Phase VI exploration next year, Agnico tries to make an acquisition in the C$6.00 to C$8.00 range. This scenario should play out within 18 months and I think the likelihood of this happening is very high. The alternate scenario is no bid, and it’s a 5 bagger from here. Don’t make me say told U.

Positioning

This is definitely a long-term play. Best for long-term ports. It is 20% of my personal long-term port. Members of my family also hold it, with a 10 to 20% portfolio allocation. Upside potential is huge. No hard timelines, buy it and forget it. It is a multibagger from here. One thing to note is that this stock is largely detached from the broader markets since it is results driven. From my observation it holds up decently well in downturns and corrections.

Leave your comments down below and let’s discuss!

Love U,

dick

An Important Disclaimer: Please Read Carefully

Investing and trading involve significant risk, including the potential loss of principal. Neither Dick Capital nor any of its affiliates are financial advisors, investment advisors, broker-dealers, or any other type of licensed financial professional. All content published by Dick Capital, whether on this Substack or in the private Discord, is for educational and entertainment purposes only and should not be construed as financial advice. Nothing you read here is a recommendation to buy, sell, or hold any security. Do your own research (DYOR). The analysis shared represents the views of Dick Capital and may change without notice. At any time, Dick Capital may hold positions in the stocks or assets discussed. By subscribing to and reading this Substack, or by participating in the private Discord, you agree that you are fully responsible for any and all investment decisions you make.

We are doing the same.

First target is reached.